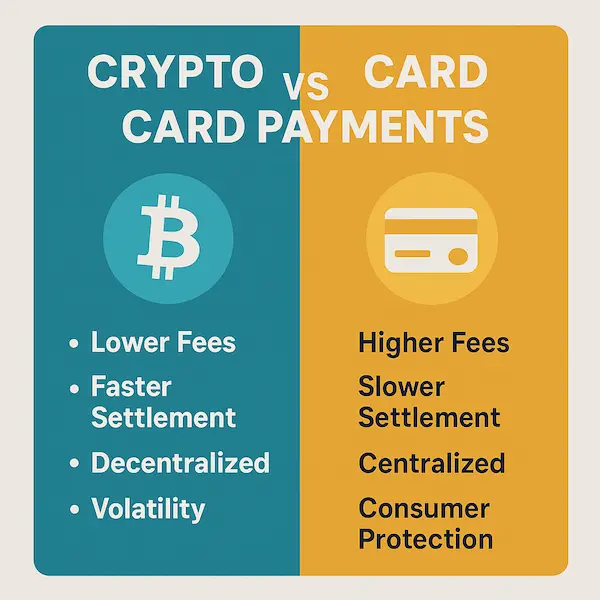

Payment Processing Using Blockchain means using blockchain technology in the payment field. Blockchain technology has the potential to simplify digital payments. By lowering the number of middlemen, it expedites transactions and further lowers the price of using third-party services.

Satoshi Nakamoto, the pseudonym of one or more people, published “Bitcoin: A Peer-to-Peer Electronic Cash System” in 2008. This document gave birth to the idea of Blockchain, the technology that underpins Bitcoin. Its revolutionary purpose is to remove intermediaries (like banks) from payment processes and transfer money directly from buyer to seller. Since then, projects related to Blockchain and finance have proliferated.

Since bitcoin incurred, it has attracted attention from the media, governments, regulators and investors alike, owing to its innovative features and colossal price appreciation. However, Bitcoin has been accompanied by very high volatility and uncertainty surrounding the future price behaviour of this popular cryptocurrency.

Every machine running the Bitcoin protocol can access the Blockchain, which allows all users to view every transaction. Once the buyer verifies they possess the bitcoins linked to their address, the seller completes the transaction and records it in the public blockchain ledger. The privacy of both parties is maintained since an address cannot be directly traced back to a specific individual.

Unlike traditional coins or paper money, cryptocurrencies do not have a physical form and lack intrinsic value. Their worth is not endorsed by any government. The decentralized nature of cryptocurrencies offers significant advantages, such as preventing the loss of resilience due to the failure of a central computer system and avoiding the concentration of power, which could otherwise allow a single entity to control the system.

Although distributed ledger technology includes blockchains, not all distributed ledger technologies are blockchains, blockchain is a particular type of distributed ledger technology that builds a linear, impenetrable chain of blocks using consensus processes and cryptographic hashing. A distributed ledger that documents every transaction ever made is known as a blockchain in the context of cryptocurrency. Blockchains include, for example, Bitcoin, Ethereum, and others.

Contents

1. Blockchain Network Types

Blockchain networks can be divided into two categories: private and public.

- Public Blockchain: There are no limitations on accessing the public Blockchain. Sending transactions and becoming a network validator is possible for anyone with an internet connection.

- Private Blockchain: No one is permitted to join the Private Blockchain unless invited by the network administrator. Accessibility for participants and validators is limited. Businesses that are interested in blockchain technology but find the control level offered by public networks inconvenient are drawn to this kind of Blockchain.

2. What is Payment Processing Using Blockchain?

Payment Processing Using Blockchain techonology are referred to as blockchain payments or blockchain payment systems. They are expected to be inexpensive, safe, and swift, enabling money transfers regardless of the sender and recipient’s distance from one another.

Furthermore, blockchain payments aren’t limited to cryptocurrency transactions; the system may Accept crypto on WooCommerce in a variety of currencies, including US and Canadian dollars.

3. What is Cryptocurrency?

A cryptocurrency is a form of digital currency that is inherent to blockchains and is sometimes referred to as a crypto-currency or crypto. It is not backed or managed by a single central entity, like a bank or government, and functions as a medium of exchange over a decentralized computer network. Stablecoins like USDT or Bitcoin and Ethereum are two examples.

Having a bitcoin address, which has a balance listed on the Blockchain, is what it means to hold cryptocurrency, such as bitcoins. Distributed ledger technology infrastructure is used by cryptocurrencies to facilitate safe, decentralized, and transparent transactions.

4. What is a Cryptocurrency Wallet?

The combination of a user’s public addresses and private key is called a crypto wallet. A user needs both to send and receive cryptocurrency transactions and monitor their balance.

Creating a new user on a blockchain is equivalent to creating a new pair of private and public keys for a cryptocurrency wallet. Numerous applications are available that take the data in a wallet and facilitate currency management for the user. A variety of cryptocurrency coins can be stored in a single wallet, or users may want to have separate wallets for each currency.

5. Blockchain Applications

Blockchain is experiencing rapid growth in today’s era, with its value projected to soar from 7 million USD in 2022 to a staggering 94 million USD in 2027.

Take a very typical example of blockchain application in the financial sector. With its superior features, blockchain helps cross-border payments be made faster, safer, less costly and more transparent in asset management. Or apply blockchain in the retail sector, payment intermediaries, supply chains, healthcare, etc. Blockchain fully supports and allows data sharing safely, transparently and quickly. Therefore, blockchain can be applied in all fields such as:

- Finance and banking

- Cryptocurrency

- Cybersecurity

- Healthcare

- Real estate

- Supply chain and logistics

- Insurance

- Voting and governance

- Internet of Things (IoT)

- Retail

- Media and Advertising

- Energy management

- Copyright protection

- Sustainability and Impact Investing

- Non-fungible tokens (NFTs)

6. Let’s check examples of using blockchain in a payment gateway

How Verify the payment process by using Blockchain in e-commerce

The suggested blockchain e-commerce payment system consists of the merchant, the customer’s smartphone app, and the blockchain system.

- After selling its goods and services, the business asks the client to pay with a blockchain cryptocurrency. Because the merchant might request payment using a QR code that appears in the customer’s web browser rather than through a different online channel, this process is denoted by a dotted line. Also, it depends on the system the merchant uses such as OTP, or any additional method applied as requested by the system.

- The merchant asks the blockchain system for confirmation to verify whether the customer has actually made the payment.

- After purchasing goods and services, the buyer scans the QR code to pay the seller. The payment request is sent to the blockchain system, which houses the transaction ledger, rather than to the merchant directly.

- The payment amount is raised in the merchant’s account and subtracted from the customer’s account by the blockchain system. After carrying out this transfer between the accounts, the blockchain system sends the outcomes to the merchant. The merchant delivers the purchased item or offers the customer the purchased service after verifying that the payment was received correctly.

Another example of using blockchain in cross-border payments.

Applying blockchain in this payment activity will help eliminate intermediaries and make international money transfers faster and cheaper. Let’s check out how the cross-border payment journey.

Here it is a consumer cross-border payment journey:

- The merchant provides a cryptocurrency payment option at the checkout or another payment channel.

- After choosing this option, the consumer agrees to the exchange rate, chooses the digital currency they wish to use for payment, and is given the merchant’s public address.

- The consumer pays the blockchain processing cost, accesses their cryptocurrency wallet, and transfers money to the merchant’s public address.

- To ensure that the customer has enough funds to complete the transaction, transaction requests are sent to the blockchain and checked by nodes

- After being submitted to a block, the transaction is awaited validation by miners.

- Usually, three nodes must certify a verified block before a transaction is authorized.

- The blockchain records the completed transaction.

7. Pros and Cons of the Blockchain Payment

Pros

- Decentralization: Transactions are carried out via a consensus method rather than a third party or reliable middleman.

- Transparency and trust: A distributed, public, time-stamped assets ledger, or general ledger, Blockchain records all completed or processed network transactions and enables computer users to verify each one so that no double calculations occur.

- Unchangeable: Several parties, whether private, public, or semi-private, may share this general ledger.

- Accessibility: The system can be placed at the maximum level of accessibility if it has a peer-to-peer network and all nodes have access to a copy of the most recent data. The network can still function even if some nods disappear or are unavailable.

- Simplifying and safeguarding existing models: Current models are highly erratic in certain sectors, like the financial or medical sectors. For various entities to maintain their databases. The inherent differences between systems cause this problem (lack of integrity and order), making data sharing extremely challenging. However, Blockchain can be utilized as a single general ledger that all parties are ready to use. This technology can make present models easier and safer by reducing the number of different management systems that an entity can maintain.

- Faster transactions: Because a single copy of the agreed-upon information is shared in the general ledger between the financial organizations, there is no need for the drawn-out validation, modification, and clearance process. Blockchain is a potentially significant tool in the financial industry, particularly in post-trading settlement operations.

- Saving money: Since Blockchain eliminates the need for an intermediary, overhead expenses previously incurred for the intermediary’s existence are reduced.

Cons

The distributed, peer-to-peer general ledger known as Blockchain, which contains the history of every transaction, suffers a lack of privacy. Everyone has access to all of the transaction’s elements, including the parties, subject, weight or amount, and transaction time.

- Security Model: No security measures are in place to protect user account assets. It is important to note that one of the best and most robust encryption techniques now in use is asymmetric cryptography, which is employed in Blockchain. As a result, there are no issues with the Blockchain security concept. However, no additional security layer is in place to guard against users inadvertently losing their private keys.

- Limited Scalability: There are two main objectives for the peer-to-peer blockchain technology. On the one hand, it allows anyone to add new transaction information to the histories that are collectively recorded. However, it stops any changes from being made to the information of transactions that have been recorded.

- High Cost: The issue of high cost is linked to the scalability problem.

- Legal Inadmissibility: Users can manage and transfer ownership in an open environment using blockchain technology, which is complicated. Consequently, there is ongoing debate on the existence of legal dangers.

- Inadmissibility of Users: There are still many users who have not accepted to use this tool because of concerns about factors that are disadvantageous to users.

8. Conclusion

Although blockchain technology is still in its infancy, it has the potential to alter how business is done fundamentally, and logistics is no exception. Applications for blockchain logistics can contribute to developing a more reliable system that allows suppliers and carriers to be trusted and will enable customers to invest with greater assurance. Innovative logistics solutions and/or reduced logistics costs might result from software, technology, and other technological advancements. Banks will be able to digitize the financing and payment processes in international trade transactions by implementing blockchain technology. As a result, we will see decreased expenses associated with the financing and payment methods and a more straightforward way to obtain the cash funds required to start and complete a trade transaction.

Generally the payment processing by using blockchain is the new systems on a platform must be developed by the parties involved in starting, contracting, and carrying out a trade transaction (manufacturing firms, importing firms, commercial banks, insurance companies, logistics companies, and port authorities) to adopt blockchain technology. At the same time, these activities need to be regulated, a process that has already been started in nations including the United States, Germany, France, China, Japan, and Russia. This technology will cause a paradigm shift in globalized trade, depending on how much government decision-makers, international organizations, and businesses use blockchain-based applications.

According to the World Economic Forum (2018), the use of blockchain technology will accelerate global trade growth, increasing transaction values by $1 trillion by 2025.

Visit us: https://www.facebook.com/xaigate