Choosing a crypto payment gateway may seem simple at first. But then the real questions begin to surface. Can the system settle funds directly into your bank account? Does it ensure compliance across multiple markets? Can it reduce chargeback risk while still delivering a smooth checkout experience for customers? That’s where this Triple-A crypto payment gateway review becomes valuable. Instead of treating crypto acceptance as a trend, businesses now need to evaluate it like any other payment method. In this article, XAIGATE breaks down Triple-A’s features, fees, strengths, limitations, and ideal use cases to help you decide whether it fits your payment stack in 2026.

Contents

- 1 What Is Triple-A Crypto Payment Gateway and How Does It Work?

- 2 Key Features of Triple-A Crypto Payment Gateway

- 3 Triple-A Fees and Pricing

- 4 Pros and Cons of Triple-A Crypto Payment Gateway

- 5 Who Should Use Triple-A?

- 6 Is Triple-A Safe and Legit?

- 7 Final Verdict: Is Triple-A Worth It in 2026?

- 8 FAQs – Triple-A Crypto Payment Gateway

What Is Triple-A Crypto Payment Gateway and How Does It Work?

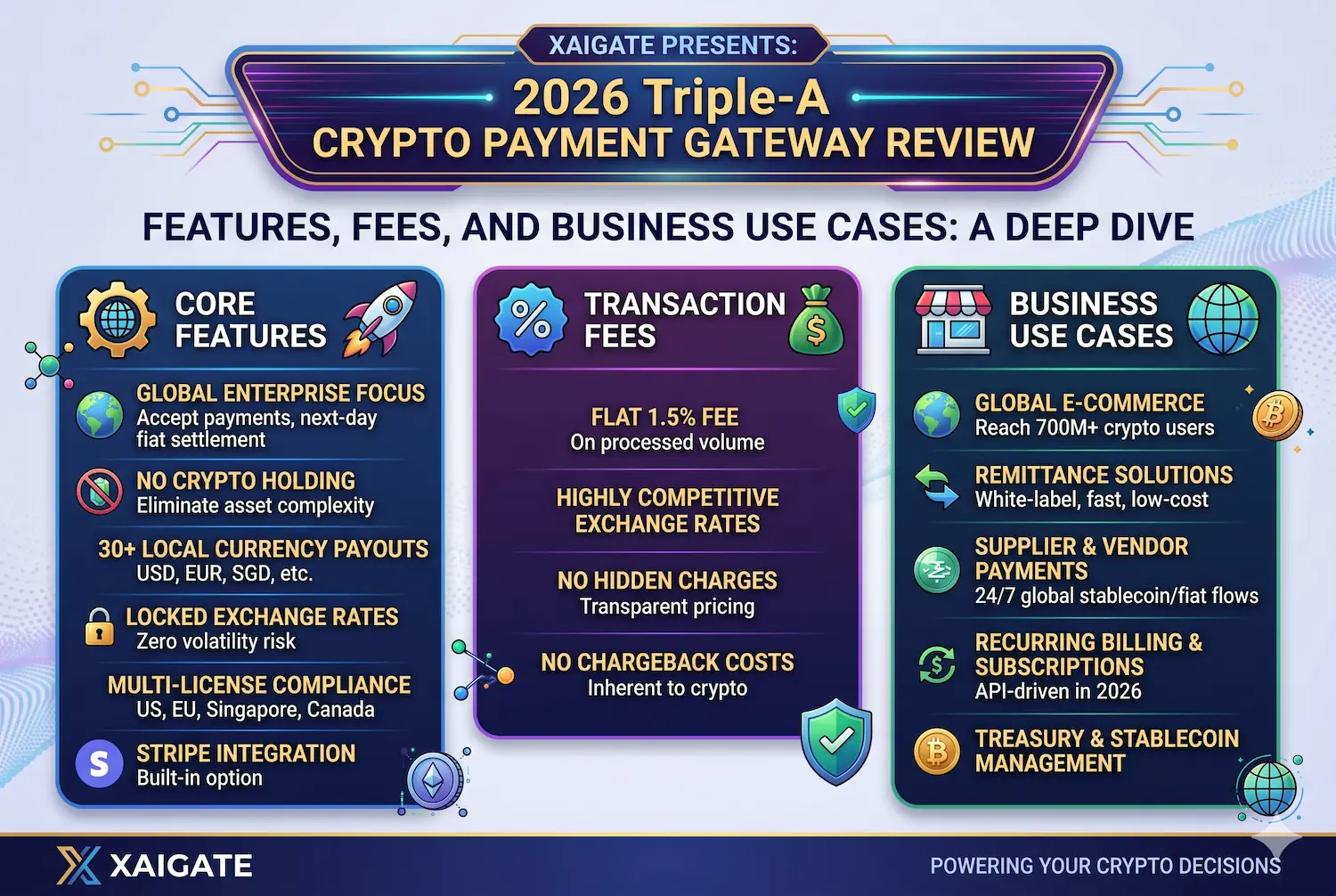

Triple-A is not positioned as a generic crypto plugin. It operates as a regulated payment institution focused on helping businesses send, receive, and convert money through stablecoin and crypto rails without forcing merchants to hold digital assets directly. The company states that it is regulated in Singapore, the United States, Europe, and Canada, with Singapore licensing under the Monetary Authority of Singapore as a Major Payment Institution.

For merchants, the operating model is straightforward. A customer chooses crypto or stablecoins at checkout, completes payment from a wallet, and the merchant can receive settlement in local currency instead of keeping crypto on the balance sheet. Triple-A also promotes locked-in exchange rates, instant confirmation, wallet compatibility, and next-day bank settlement for its digital currency payment solution. That matters for businesses that want the upside of accepting crypto without adding treasury or volatility management to finance operations.

The broader value proposition is less about speculation and more about payment efficiency. Triple-A emphasizes lower processing costs than traditional methods, cross-border reach to 140+ countries, and reduced exposure to chargeback fraud because crypto transactions are irreversible by design. For companies selling internationally, that framing is stronger than a basic accept-BTC checkout story.

Key Features of Triple-A Crypto Payment Gateway

A strong review should separate real operational value from surface-level feature lists. Triple-A does have useful merchant features, but the best way to assess them is through business impact.

Crypto acceptance with fiat settlement

One of Triple-A’s clearest strengths is the ability to let customers pay in digital currencies while merchants receive funds in local fiat. The company highlights zero-volatility exposure, direct bank settlement, and next-day payout flows. For many merchants, that is the deciding factor because it removes the need to manage wallets, internal custody policies, and token conversion workflows.

Stablecoin-first positioning

Triple-A increasingly presents itself around stablecoin payments rather than pure crypto enthusiasm. Its site emphasizes stablecoin and local currency rails, while recent product messaging around Circle Payments Network points to cross-border settlement, payroll, supplier payments, remittances, and treasury flows. That makes the platform more relevant for modern finance teams than for brands that only want a novelty crypto button.

See more: Pros and Cons of Crypto Payment Gateway in modern electronic payments

Integration options for merchants

Triple-A supports several integration routes. Businesses can use APIs, invoicing flows, and merchant dashboard tools, while WooCommerce users also have an official plugin listed on WordPress.org. The plugin description highlights wallet-agnostic payments, direct bank settlement, transaction notifications, dashboard management, and support for multiple fiat settlement currencies. That gives merchants flexibility depending on whether they need fast deployment or custom checkout control.

Dashboard and invoicing tools

The dashboard is more than a monitoring screen. Triple-A’s help center says merchants can track transactions, export records as CSV, send invoice payment requests, customize branding on payment forms, control accepted cryptocurrencies, and manage users. The invoicing tool is useful for service businesses, B2B sellers, and firms that do not want a full ecommerce integration on day one.

Triple-A Fees and Pricing

Pricing transparency is one of the first things businesses check in any crypto payment gateway review. On this point, Triple-A is solid but not perfectly detailed across all public pages.

The clearest published figure appears on its WooCommerce plugin page, which states a low settlement fee of 1.0% and no additional setup cost. The same page also says merchants can receive funds in local currency, including USD, EUR, GBP, and more than 50 other fiat currencies, with direct bank settlement.

That said, Triple-A’s main product pages focus more on business outcomes than on a full public fee schedule. So if a merchant needs exact pricing by volume, settlement type, corridor, or custom enterprise use case, a sales conversation is still likely necessary. This is not unusual in B2B payments, but it does mean Triple-A is more transparent about headline affordability than about full pricing mechanics.

Quick pricing and feature snapshot

| Area | What Triple-A publicly highlights |

| Settlement fee | 1.0% on the WooCommerce plugin page |

| Setup cost | No additional setup cost mentioned on the plugin page |

| Settlement model | Local currency settlement to bank account |

| Settlement speed | Next-day bank settlement on digital currency payments page |

| Fiat support | USD, EUR, GBP, and 50+ other fiat currencies on the plugin page |

| Merchant tools | Dashboard, invoicing, transaction tracking, user management |

| Integration options | API, invoicing, dashboard tools, WooCommerce plugin |

| Compliance positioning | Licensed or registered across Singapore, US, Europe, and Canada |

The snapshot above is drawn from Triple-A’s official product, support, and regulatory pages.

Pros and Cons of Triple-A Crypto Payment Gateway

A review becomes useful only when it makes trade-offs explicit. Triple-A has real strengths, but it is not the perfect fit for every merchant.

Pros

Triple-A’s biggest advantage is compliance-led infrastructure. The MAS listing confirms Major Payment Institution status in Singapore, and Triple-A also discloses registrations or licenses in the US, Europe, and Canada. For regulated industries, established merchants, or finance teams that need governance, this is a major differentiator.

Another strength is fiat settlement without volatility exposure. Customers can pay with crypto or stablecoins, while the merchant can receive local currency into a bank account. That reduces accounting friction and avoids the internal risk of holding crypto assets.

Triple-A also looks strong for cross-border commerce. Its site promotes coverage across 140+ countries, and its recent Circle Payments Network integration expands stablecoin-to-local-currency settlement use cases. That gives it a stronger international payments story than many basic checkout-first crypto tools.

Cons

The first limitation is public pricing depth. You can find a 1.0% settlement fee reference, but not a fully detailed public pricing matrix for every scenario. Businesses that want instant clarity on enterprise costs may find that frustrating.

The second limitation is that Triple-A’s public messaging is more stablecoin and compliant-payments oriented than crypto-native and self-custody oriented. That is great for mainstream businesses, but merchants seeking the widest possible token experimentation or a heavily developer-first self-managed stack may prefer platforms positioned more toward open crypto rails. This is an inference from Triple-A’s product framing and should be read as a strategic fit issue rather than a technical deficiency.

The third limitation is that some technical details, such as full supported network coverage, are easier to confirm through onboarding or support documentation than from simplified marketing pages alone. That means due diligence is still necessary before implementation, especially for multi-market or high-volume use cases.

See more: Insight on Crypto Payment Gateway: A Detailed Analysis of Today’s Crypto Payment Systems

Who Should Use Triple-A?

The best review question is not whether Triple-A is good in general. It is whether Triple-A is good for your business model.

Best fit

| Business type | Why Triple-A fits |

| Cross-border ecommerce | Fiat settlement, broad country coverage, no chargebacks |

| SaaS and digital services | Invoice links, API options, simpler global collection |

| Marketplaces and platforms | Stablecoin payments, payout relevance, international reach |

| Finance-led enterprises | Regulatory positioning and bank-linked settlement workflows |

| Businesses entering stablecoin payments | Reduced treasury complexity and local currency delivery |

This use-case summary aligns with Triple-A’s positioning across ecommerce, marketplaces, PSPs, invoicing, and cross-border stablecoin settlement pages.

Less suitable fit

- Crypto-native merchants that want to hold digital assets rather than auto-convert them

- Businesses choosing a gateway mainly for speculative token breadth instead of settlement efficiency

- Teams that need a fully public, line-by-line enterprise pricing model before any sales discussion

These are fit-based limitations inferred from Triple-A’s official positioning around stablecoin infrastructure, local currency settlement, and compliance-first workflows.

Is Triple-A Safe and Legit?

Yes, Triple-A appears legitimate and structurally credible based on official regulatory and corporate disclosures. The strongest evidence is the Monetary Authority of Singapore directory entry showing Triple A Technologies Pte. Ltd. as a Major Payment Institution, covering services such as domestic money transfer, cross-border money transfer, merchant acquisition, and digital payment token service. Triple-A’s own site also discloses licensing or registration details across Singapore, France, the United States, and Canada.

From a merchant risk perspective, the safer part of the model is that businesses can access crypto and stablecoin payment demand without directly taking custody of assets. Combined with locked exchange rates, next-day bank settlement, and the absence of chargeback exposure, that creates a risk profile many mainstream businesses can actually operationalize.

Final Verdict: Is Triple-A Worth It in 2026?

In this Triple-A crypto payment gateway review, the answer is yes for the right type of business. Triple-A is not trying to be the most experimental crypto gateway in the market. It is trying to be one of the most practical. Its strongest advantages are regulatory credibility, stablecoin-friendly infrastructure, local currency settlement, cross-border relevance, and tools that work for both integrations and invoice-driven payment collection.

For most global merchants, SaaS brands, marketplaces, and modern cross-border businesses, Triple-A looks less like a niche crypto tool and more like a bridge between stablecoin infrastructure and real-world payment operations. That is exactly why it deserves a place on any serious shortlist in 2026.

Need the same article rewritten in a shorter version around 1200 words or styled more like XAIGATE’s brand voice?

For daily updates, subscribe to XAIGATE’s blog!

We may also be found on GitHub, and X (@mxaigate)!

FAQs – Triple-A Crypto Payment Gateway

1. What is Triple-A crypto payment gateway?

It helps businesses accept crypto and stablecoin payments.

2. How does Triple-A settlement work?

Customers pay in crypto; merchants can receive local fiat.

3. Is Triple-A regulated?

Yes, it highlights regulatory coverage in multiple markets.

4. Does Triple-A support stablecoins?

Yes, stablecoin payments are part of its core positioning.

5. Can Triple-A reduce volatility risk?

Yes, fiat settlement helps merchants avoid holding crypto.

6. Does Triple-A support WooCommerce?

Yes, it has WooCommerce plugin support.

7. What merchant tools does Triple-A offer?

APIs, invoicing, dashboard tools, and transaction tracking.

8. What is Triple-A’s published fee?

Its WooCommerce page mentions a 1.0% settlement fee.

9. Who should use Triple-A?

Ecommerce, SaaS, marketplaces, and cross-border businesses.

10. What should merchants compare first?

Compare fees, settlement, countries, APIs, support, and compliance.